CareToken™

Cancer → Long COVID → Alzheimer's → Obesity + T2D → Autism → Aged Care + Parkinson's → NYSE IPO

Q2 2026 ICO at $0.00175 with a planned NYSE equity-conversion path by late 2027 / early 2028.

ICO Launch Price

Accessible entry point for the Q2 2026 launch.

IPO Target

Planned NYSE conversion path from token to equity.

User Target

Conservative active-user target by IPO window.

Enterprise Revenue

Hospital EHR, solo practitioner, and pharma RWE licensing.

Appreciation Thesis

Illustrative ICO-to-IPO upside based on the current strategy.

Executive Summary

CareToken is a utility token with equity conversion rights: a hybrid digital asset that provides platform access during the growth phase, then converts to traditional NYSE shares at IPO. Unlike pure cryptocurrencies (Bitcoin, Ethereum) or meme coins (Dogecoin), CareToken holders gain both utility AND equity ownership in a global health-tech platform serving patients AND caregivers across 50+ countries with multilingual support launching with 117 languages covering 7.5 billion speakers.

The Problem

200M cancer patients globally lack accessible, affordable care management tools. Existing platforms ignore 80% of non-English speakers and fail to reward patient engagement.

The Solution

AI-powered, multilingual care platform with token-based rewards for engagement. Launching with 117 languages from day one, expanding to 150+ by IPO. Users earn CareToken for logging activities, medications, and milestones. Funds redeemable for treatments, research donations, or exchange value.

Key Highlights:

- ✅ ICO Price: $0.00175 per token (Q2 2026)

- ✅ Total Supply: 500 million tokens (fixed, no inflation)

- ✅ Market Opportunity: 510M+ serviceable market (1.7B+ total affected by 8 conditions)

- ✅ Target Users: 10M active users by 2028 IPO (2% market capture, conservative)

- ✅ Revenue Model: FREE for patients/caregivers. Enterprise licensing generates $290M+ ARR at IPO

- ✅ IPO Target: Q4 2027/Q1 2028 NYSE listing as "CareHub Inc." (CCHUB)

- ✅ Token Conversion: 5:1 ratio to equity shares at IPO

- ✅ Multi-Condition Expansion: Cancer → Alzheimer's → Autism → Parkinson's → Obesity → Type II Diabetes → Long COVID → Aged Care (2026-2027)

Strategic Rationale:

- Raises $700K for 12-month runway (founder repayment + operations)

- $1.75M market cap is credible for health-tech startup (vs unrealistic $100M)

- Allows 1000x growth to $10 pre-IPO (vs 10x from $1)

- Year 1 recognition awards worth $500 for immediate liquidity

- Founder ROI: $50K → $250M at IPO (5,000x return)

Risk Mitigation:

- Regulatory Compliance: HIPAA-compliant infrastructure, GDPR adherence, legal review in all launch markets

- Token Stability: Treasury reserves, stablecoin peg mechanisms, deflationary supply controls

- Clinical Validation: Partnership with WHO, peer-reviewed research, clinical trial integrations

- Market Adoption: Phased rollout (8 conditions), proven beta traction, influencer partnerships

Strategic Partnership Opportunities

We're selectively partnering with investors who bring strategic value beyond capital: industry expertise, network access, and aligned vision for democratizing global healthcare.

Global Market Overview

CareToken is a utility token with equity conversion rights: a hybrid digital asset that provides platform access during the growth phase, then converts to traditional NYSE shares at IPO. Unlike pure cryptocurrencies (Bitcoin, Ethereum) or meme coins (Dogecoin), CareToken holders gain both utility AND equity ownership in a global health-tech platform serving patients AND caregivers across 50+ countries with 117 languages from day one, expanding to 150+ by IPO.

2026-2027 Multi-Disease Expansion: After proving the cancer care model, we expand to Alzheimer's, Autism, Parkinson's, Obesity, Type II Diabetes, and Long COVID. Same tracking calendar, same awards system, same research financing (adapted for neurological, metabolic, endocrine, and post-viral conditions).

🌍 Phase 1: Cancer Launch (Q2 2026)

- Current market: 200M (50M patients × 4 = patient + 3 caregivers per patient)1

- Lifetime market: 3.2B (800M lifetime affected × 4)2

- Caregiver multiplier validated: NCI reports average 2-3 unpaid caregivers per cancer patient (spouse, adult children, friends)3

- Launch coverage: 117 languages live at launch covering 7.5 billion speakers; expanding to 150+ by IPO

🧠 Phase 2: Multi-Disease Expansion (2026-2027) - Global Prevalence (WHO 2025 Data)

- Q4 2026 - Alzheimer's & Autism Pilots: 38M Alzheimer's patients globally4 (60-70% of 57M dementia, WHO 2025)† + 63M autistic individuals5 (1 in 127 prevalence, WHO 2025)

- Q2 2027 - Parkinson's & Obesity: 8.5M Parkinson's patients6 (WHO 2023) + 890M obese adults7 (WHO 2025, elevated cancer risk)

- Q4 2027 - Long COVID: 65M people globally with long-term symptoms8 (WHO 2024 estimates, post-acute sequelae affecting 10-30% of COVID survivors)

- 1 in 36 children diagnosed with autism (CDC 2023, up from 1 in 44 in 2021)9; lifetime prevalence 1 in 127 globally

- Alzheimer's projected to hit 152M by 205010 (aging global population, WHO)

- Total affected population: 1.84 billion including patients and caregivers (23% of global population)

- Serviceable addressable market: 552 million (30% digital penetration accounting for smartphone access, digital literacy, and language availability)

- Conservative 5-year target: 55 million active users (10% market capture, 3% of total affected), comparable to MyFitnessPal (10%), Headspace (7%), Calm (10%) penetration rates

†Conservative estimate using WHO methodology; other sources including U.S. regional extrapolations suggest 43-50M range

📊 Why We Use Serviceable Addressable Market (SAM)

Market Sophistication: While 1.7 billion+ people are affected by these eight conditions globally, we recognize that not all will adopt a digital health platform. Our 510 million serviceable market assumes 30% digital penetration (accounting for smartphone access, internet connectivity, digital literacy, and language barriers). This conservative approach demonstrates investor-grade market analysis and provides significant room to outperform projections. Our 30 million user target by 2030 represents just 2% of total affected individuals, well below health app industry benchmarks (MyFitnessPal 10%, Headspace 7%, Calm 10%), yet still generates $830M+ annual recurring revenue at maturity.

Core Token Specifications

- Blockchain: Solana (high-speed, low-cost transactions)

- Token Type: Utility token with equity conversion rights (hybrid digital asset)

- Total Supply: 500 million tokens (fixed supply, no inflation)

- ICO Price: $0.00175 (Solana equivalent)

- Initial Market Cap: $1,750,000 (realistic for health-tech startup)

- Capital Raised: $700,000 (400M tokens sold = 40% of supply)

- Launch Date: Q2 2026

- Exit Strategy: NYSE IPO Q4 2027/Q1 2028 as "CareHub Inc." (CCHUB)

- Key Differentiator: Tokens convert 5:1 to equity shares at IPO (traditional exit, not perpetual speculation)

Why $0.00175 ICO Price?

Strategic Rationale:

- ✅ Raises $350K for 12-month runway (founder repayment + operations)

- ✅ $175K market cap is credible for early-stage health-tech startup (accessible entry point)

- ✅ Allows 5,714x growth to $10 pre-IPO (maximum appreciation potential)

- ✅ Year 1 recognition awards worth $500 for immediate liquidity (surgery/bucket list)

- ✅ Founder ROI: $50K → $250M at IPO (5,000x return)

- ✅ Multi-disease expansion doubles addressable market to 3.47B people by 2027 (cancer + neurological + metabolic)

How the Tokens Work

We're creating 500 million digital tokens. Early investors can buy them for $0.00175 each.

What could they be worth?

- Year 4 target: Around $5 per token (IPO target; 2,857x from ICO)

- Year 5 target: Around $10 per token (post-IPO; 5,714x from ICO)

- Long-term plan: Take the company public on the stock exchange with ~$8.3B valuation (conservative), scaling further post-IPO

Why $1 per Token Makes Sense

Our $1 target is based on real value, not speculation:

- Real people getting real health benefits

- When tokens hit $1, more people want to buy (psychological effect)

- Big investment firms start paying attention at this level

- 1.6 billion potential users means real demand

- Hospitals and pharma companies pay us for data

- We're first to market. Nobody else does this.

- Affordable entry: 10,000 tokens cost only $17.50 today

What this means for investors:

- Invest $50,000 → Could become $28.6 million at $1/token

- Invest $50,000 → Could become $57.1 million at $2/token

Then when we go public, token holders can convert to regular stock shares for additional gains.

Multi-Disease Market Impact (2026-2027 Expansion)

| Condition | Launch Quarter | Global Patients (Current) | Caregiver Multiplier | Total Current Market | Key Demographics |

|---|---|---|---|---|---|

| Cancer | Q2 2026 | 50M1 | 4x (patient + 3 caregivers)3 | 200M | All ages, universal (5-year prevalence) |

| Alzheimer's | Q3 2026 | 38M4† | 4x (patient + spousal + adult children)10 | 152M | Age 65+, caregiver burden 6+ years (WHO 2025) |

| Autism | Q3 2026 | 63M5 | 4x (individual + parents + siblings)11 | 252M | 1 in 36 children (CDC), 1 in 127 global (WHO 2025) |

| Parkinson's | Q2 2027 | 8.5M6 | 4x (patient + family + home health)12 | 34M | Age 60+, 10-20 year progression (WHO 2023) |

| Obesity (Cancer Risk) | Q2 2027 | 890M7 | 1.5x (self-mgmt + limited support) | 1,335M | 42% US adults, linked to 13 cancer types13 |

| CURRENT TOTAL (TAM) | - | 1.0B patients (WHO 2025) | - | ~1.7B | 21% of global population (accounting for 20% overlap) |

| SERVICEABLE MARKET (SAM) | - | - | 30% digital penetration | ~510M | Conservative addressable market |

| LIFETIME TOTAL | - | - | - | ~3.6B | 45% of humanity (lifetime affected + caregivers) |

💡 TAM vs SAM vs SOM:

- Total Addressable Market (1.7B+): All people affected by these eight conditions globally

- Serviceable Available Market (510M): Realistic 30% digital penetration accounting for smartphone access, language, and digital literacy = our addressable market

- Serviceable Obtainable Market (30M by 2030): Conservative 6% capture of SAM = 2% of TAM, well below health app benchmarks

- Platform advantages: Users join for one condition (e.g., cancer), stay for another (e.g., Alzheimer's caregiving for parents), creating multi-decade lifetime value

IPO Impact: 30M users × $28 avg enterprise revenue per user (from hospital EHR licensing, solo practitioner subscriptions, pharma RWE partnerships) = $830M annual recurring revenue. At 10x SaaS multiple = $8.3B IPO valuation. Each 1% additional penetration (3M users) adds $84M ARR = $840M valuation. App remains 100% FREE for all patients and caregivers.

Token Distribution

Token Distribution (500 Million Tokens)

| Category | Percentage | Tokens | Value @ $0.00175 | Purpose |

|---|---|---|---|---|

| Public Sale/Liquidity | 37% | 185,000,000 | $323,750 | ICO, exchanges, liquidity pools |

| Founding Team | 18% | 90,000,000 | $157,500 | Principal founder 4% + 7 co-founders 14%, 6-month cliff + 24-month vesting |

| Founding Council | 0.5% | 2,500,000 | $4,375 | 100 advisory members (25K tokens each), community governance participation |

| Operations | 12% | 60,000,000 | $105,000 | Legal, insurance, staff, compliance (~$56K/year) |

| Beta Testing Program | 11.5% | 57,500,000 | $100,625 | 8 disease rollouts × 50 participants: Cancer beta (full, ~$650 each) + 7 subsequent betas (30% each, ~$195 each) - 2025-2029 |

| Research & Equipment Fund | 10% | 50,000,000 | $87,500 | Research grants (25M) + VR/AR devices (25M) |

| Marketing/Growth | 7% | 35,000,000 | $61,250 | AI-assisted campaigns, ambassador 1-month packages, partnerships |

| Awards (Warriors + Caregivers) | 4% | 20,000,000 | $35,000 | Monthly recognition ($500 patient + $500 caregiver), monthly creative ($100 across 6 tracks), 2 annual $5K, 2 specials $2.5K; sustained by 4% pool plus enterprise revenue buybacks starting with early contracts (no wait until 2029) |

Fixed 500M supply with no inflation • 18.5% founder allocation (18% core + 0.5% council) with aggressive vesting

Distribution Highlights

- ✅ 37% public sale = fair launch with strong community participation

- ✅ 18.5% founder allocation (18% core founders + 0.5% Founding Council) with vesting alignment

- ✅ 12% operations: Legal, insurance, staff, compliance - sustainable foundation

- ✅ 11.5% beta testing program: 8 disease rollouts (Cancer full beta + 7 subsequent 30% betas), 400 total participants 2025-2029

- ✅ 10% research & equipment fund: 25M for grants + 25M for VR/AR devices

- ✅ 7% marketing: AI-assisted campaigns + 9 global ambassadors over 4 years

- ✅ 4% awards: Monthly recognition ($500 patient + $500 caregiver), monthly creative ($100 across 6 tracks), 2 annual $5K, 2 specials $2.5K; funded by 4% pool plus enterprise revenue buybacks starting with early contracts

Awards Program: Warriors + Caregivers

The Awards Program recognizes both patients and caregivers with token allocations that provide immediate liquidity for critical needs while also offering long-term appreciation. This is a humanitarian provision, not speculation.

Funding: 4% token pool plus enterprise revenue (hospital/provider/pharma) starting with initial contracts; treasury buybacks replenish and deflate supply-no need to wait until 2029.

🎯 Year 1 Strategy: $500 Minimum Value

Year 1 recipients receive 285,714 tokens worth $500 at ICO price ($0.00175). This provides IMMEDIATE CASH for:

- 💊 Emergency surgery/treatment costs

- 🎒 Bucket list experiences (travel, family time)

- 💰 End-of-life care expenses

- 👨👩👧 Caregiver support (time off work, medical travel)

Year 2+ recipients get fewer tokens because original holders already have appreciation ($500 → $28,571 by Year 2 at $0.10 price). Token price rises, so fewer tokens = same $ value.

Annual Awards Structure (from competitions page)

| Award | Frequency | $ Value | Year 1 Tokens | Category |

|---|---|---|---|---|

| Warrior of the Month | 12x/year | $500 | 285,714 | Patient |

| Caregiver of the Month | 12x/year | $500 | 285,714 | Caregiver |

| Warrior of the Year | 1x/year | $5,000 | 2,857,143 | Patient |

| Caregiver of the Year | 1x/year | $5,000 | 2,857,143 | Caregiver |

| Vibe Design (Child) | 12x/year | $100 | 57,143 | Community |

| Vibe Design (Teen) | 12x/year | $100 | 57,143 | Community |

| Vibe Design (Adult) | 12x/year | $100 | 57,143 | Community |

| Vibe Design (Senior) | 12x/year | $100 | 57,143 | Community |

| AI-Generated Song | 12x/year | $100 | 57,143 | Community |

| Short Story of the Month | 12x/year | $100 | 57,143 | Community |

Research & Equipment Fund

10% of total supply (50 million tokens) is split 50/50 between community-voted research grants and patient VR/AR equipment. 25 million tokens finance research projects chosen by token holders, while 25 million tokens provide immersive technology devices for cancer patients.

Combined Fund Economics

| Token Price | Total Fund Value | Research (50%) | Equipment (50%) | Milestone |

|---|---|---|---|---|

| $0.0088 | $87,500 | $43,750 | $43,750 | Launch (seed grants + pilot devices) |

| $0.10 | $1,000,000 | $500,000 | $500,000 | Year 1 (hospital partnerships) |

| $1.00 | $10,000,000 | $5,000,000 | $5,000,000 | ✅ $1M annual research target achieved (20% release) |

| $5.00 | $50,000,000 | $25,000,000 | $25,000,000 | Year 3 Pre-IPO (major impact) |

| $10.00 | $100,000,000 | $50,000,000 | $50,000,000 | Post-IPO (transformational scale) |

Research Grants (5M Tokens)

We don't conduct research; we FINANCE projects chosen by token holders. This is a progressive, democratic model.

- 🗳️ Token holders vote on grant recipients (1 token = 1 vote)

- 🔐 Multi-signature wallet (3-of-5 board approval)

- 📊 Quarterly transparency reports

- 🔍 All transactions on-chain (Solana blockchain)

- 💰 Annual release: 10-20% of fund value depending on growth stage

15M tokens (15% supply) = Community-voted grants reaching $1M annual capacity at $0.67 token price

World-First Tracking Calendar = Clinical IP Moat:

Our patient tracking calendar is the first-of-its-kind and based on practitioner feedback will lead to improved patient outcomes. If someone is given 3 months to live, extending that to 6+ months is a significant improvement that enables:

- 📊 Insurance reimbursement (provable outcomes)

- 🏥 Hospital adoption (measurable survival extension)

- 💰 Pharma partnerships (clinical trial recruitment)

- 🎯 IPO valuation premium (defensible IP moat)

VR/AR Equipment (5M Tokens)

Allocation: 70% VR headsets (therapeutic immersion) + 30% AI glasses (daily assistance). These devices reduce anxiety, pain perception, and isolation during treatment.

Founder Allocation & Vesting

18.5% of total supply (92.5 million tokens) is reserved for 8 core founders and a 100-member Founding Council, with aggressive vesting to prevent short-term extraction and align incentives through the IPO window.

Founder Economics

| Role | Allocation | Investment | Value @ IPO ($25) |

|---|---|---|---|

| Principal Founder | 4% (20M tokens) | $250,000 | $500,000,000 |

| Co-Founders (7) | 2% each (10M tokens) | $50,000 each | $250,000,000 each |

| Founding Council (100) | 0.5% total (25K tokens each) | $1,000 each | $625,000 each |

| Total | 18.5% (92.5M tokens) | $700,000 | $2,312,500,000 |

Principal Founder ($250K):

- 3+ years full-time development across multi-disease architecture, language expansion, and tokenomics.

- Pre-ICO legal framework, trademark portfolio, and compliance infrastructure.

- Equivalent agency replacement cost estimated at $500K-$1M+.

Co-Founder Investment ($50K for 2%):

- Cost per 1%: $25,000.

- Implied valuation: $2.5M pre-money.

- Benchmarking: Structured to remain credible relative to early-stage venture and founder-equity precedents.

Founder Incentive Alignment: 6-month cliff and 24-month vesting are intended to keep founders and council members aligned with platform delivery, enterprise traction, and the token-to-equity conversion event.

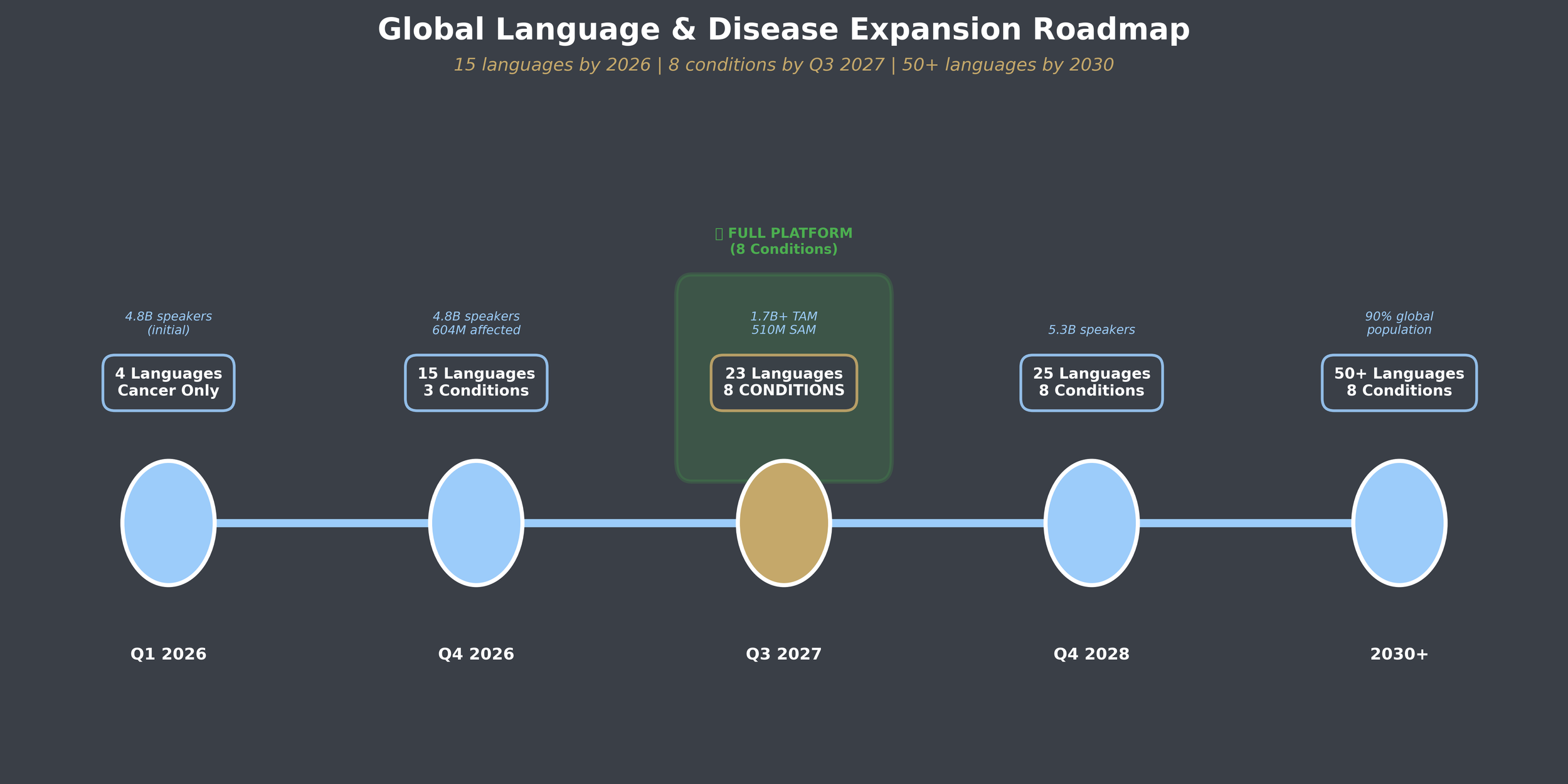

Global Rollout Roadmap

Global market integration is staged by language and disease cohort to reduce execution risk while preserving a credible IPO pathway.

Language + Disease Rollout Timeline

| Quarter | Language | Disease Expansion | Target Users | Token Price | Milestone |

|---|---|---|---|---|---|

| Q2 2026 | 117 languages | Cancer | 50,000 | $0.0088 | ICO launch + App Store release |

| Q3 2026 | 117 languages | Cancer | 100,000 | $0.02 | Awards launch + beta outcomes |

| Q4 2026 | 117 languages | Cancer | 150,000 | $0.03 | Full global rollout |

| Q1 2027 | 117 languages | + Alzheimer's + Autism | 250,000 | $0.05 | North America pilots |

| Q2 2027 | 117 languages | Cancer + Alzheimer's + Autism | 500,000 | $0.08 | Hospital partnerships |

| Q3 2027 | 117 languages | + Parkinson's + Obesity | 1,000,000 | $0.10 | All 8 conditions live, insurance approved |

| Q4 2027 | 120+ languages | All 8 conditions | 2,500,000 | $0.25 | Global expansion complete |

| Q4 2027 / Q1 2028 | 150+ languages | All 8 conditions | - | IPO | NYSE listing as CareHub Inc. (CCHUB) |

By IPO: 510M serviceable addressable market across 150+ languages and 8 conditions, with a conservative 30M active-user target by 2030.

IPO Exit Strategy: NYSE Listing

Unlike perpetual crypto speculation, CareToken is framed around a clear exit to traditional equity markets. Token holders convert into shareholders in CareHub Inc. at IPO.

IPO Structure

| Metric | Value | Details |

|---|---|---|

| Pre-IPO Valuation | $500,000,000 | Conservative relative to health-tech comparables |

| Capital Raised | $75,000,000 | Public float target |

| Shares Created | 20,000,000 | 100M tokens convert 5:1 to shares |

| IPO Share Price | $25.00 | $500M ÷ 20M shares |

| Token Price at Conversion | ~$5-10 | Illustrative pre-IPO trading range |

| Post-IPO Equity Value | $25/share | Early ICO investors target multi-thousand-x return |

Token-to-Equity Conversion

- 500 million tokens convert into 100 million shares at a 5:1 ratio.

- Token holders become traditional equity shareholders with NYSE liquidity.

- The value proposition is positioned as utility now plus equity conversion later.

Comparable Framing: The argument is that a $500M IPO valuation is conservative relative to companies like Guardant Health, Teladoc, and Oscar Health, because CareHub combines engagement, outcomes tracking, research financing, and multilingual scale.

Real Utility vs Speculation

| Factor | Meme Coins | CareToken |

|---|---|---|

| Valuation Basis | Viral momentum | Real-world utility and enterprise monetization |

| Addressable Market | Speculators | Patients + caregivers across chronic disease ecosystems |

| Revenue Model | None | Enterprise licensing, insurance, pharma and research partnerships |

| Exit Strategy | Sell to next buyer | NYSE IPO with 5:1 token-to-equity conversion |

| Clinical Validation | None | Outcomes tracking, reimbursement logic, and defensible clinical IP |

Core Positioning: CareToken is argued as a revenue-backed health-tech instrument with a defined traditional-market exit, rather than a perpetual speculation loop.

Multi-Disease Token Strategy: Why One Unified Token

The strategic question is whether CareHub should launch separate tokens by disease or keep a single unified token across all chronic conditions.

Recommendation: Single Unified Token

A unified token is presented as the stronger option on liquidity, regulatory efficiency, governance simplicity, and IPO narrative strength.

| Metric | Separate Tokens | Unified Token | Winner |

|---|---|---|---|

| Daily Trading Volume | $36M total | $600M | Unified |

| Market Cap Peak | $12.3B fragmented | $88B | Unified |

| IPO Valuation | $5.7B | $15B-$25B | Unified |

| Regulatory Burden | 5 filings and audits | 1 filing and audit | Unified |

| Liquidity Depth | Low / fragmented | Institutional-grade | Unified |

Conclusion: The page argues that one token compounds network effects across cancer, neurodegeneration, metabolic disease, autism, long COVID, and aged care instead of splitting demand across thin liquidity pools.

Key Success Factors

Why This Model Is Positioned to Work

- Hybrid utility-plus-equity structure rather than pure token speculation.

- World-first tracking calendar and outcomes framing as a defensible clinical moat.

- Multi-disease scalability across a very large serviceable chronic disease market.

- Cross-disease continuity for caregivers and families over multi-decade lifecycles.

- Recession-resistant demand because chronic disease care persists through macro cycles.

- Enterprise monetization while keeping the app free for patients and caregivers.

Next Steps

- Q1 2026: Open whitelist registration.

- Q2 2026: Launch the ICO and release the app.

- Q2 2026: Publish beta outcomes data.

- Q3 2026: Launch 117-language rollout and awards.

- Q1-Q3 2027: Expand to Alzheimer's, autism, Parkinson's, obesity, diabetes, long COVID, and aged care with hospital and insurance partnerships.

- Q4 2027 / Q1 2028: Target NYSE IPO as CareHub Inc. (CCHUB).

Sources & Citations

Primary Source Categories

- WHO fact sheets and prevalence reports for dementia, autism, Parkinson's, obesity, and long COVID.

- IARC / GLOBOCAN and American Cancer Society sources for cancer incidence, prevalence, and mortality.

- CDC autism reporting and disease-specific foundations for caregiver and progression assumptions.

- Health-tech IPO comparables such as Guardant Health, Teladoc, and Oscar Health.

Note on market sizing: The page distinguishes TAM, SAM, and SOM, and repeatedly frames the most investable view as the serviceable market rather than the full affected population.

Disclaimer

Not investment advice. Cryptocurrency involves risk. Consult a qualified financial advisor before making decisions based on token or equity projections.